For those of you that follow me on LinkedIn and were looking forward to a piece on C-suite hiring, you’ll have to wait. My ADHD got the best of me at the DykemaDSO conference and I simply had to head off on another tangent. More on hiring next time around. Maybe.

Much has been made about the influx of private capital into the dental space. Some may call it the demonization of a previously perfected healthcare model. Many were indifferent at onset. Now, in increasingly greater numbers, people are beginning to see both the evolution of that capital influx and the resulting impact it can have when allowed to dominate an acquisition landscape. While nobody at this point is denying the profound impact it has had, few people truly understand what an ongoing equity play looks like after the first, second and now the third cycle.

Simplification

Let’s back up for a second to simplify this. Private equity is essentially a private fund, comprised of a group of high net worth individuals/organizations placing their capital into a “fund.” The PE group provides a fund manager(s) who utilize that capital to purchase all kinds of different assets. The profits from those assets get paid out as essentially what could be considered “dividends,” or an immediate coupon return. However, the true payoff is on the back end when the fund manager pulls together all of these assets he/she have spent years developing, and sell the bulk of them at a premium. That premium is, in large part, passed along to the original investors and they cash out of the fund with a very nice return. The capital cycle for a fund like this is generally 5-7 years with very few variations on that time frame.

Dry Powder

Why would the above explanation be important? Dry powder. It’s a term long used in the PE space describing the number/quality of investible assets within a space. To draw a direct parallel, the medical industry began consolidating 20 years ago. Fifteen years and a couple of equity cycles later, and you have a largely consolidated medical marketplace, which has in essence run out of investable dry powder. To further drive the narrative, it is that fact that has driven PE capital into the dental space faster than anything else. During the medical consolidation of the 90s and 2000s, everyone made money by pulling together good, mediocre and flat out crappy practices, picking up basic modern efficiencies, cleaning up balance sheets and selling those entities to larger hospital groups. However, with much of that work largely completed and returns diminishing, PE looked elsewhere for “dry powder” markets to pump capital into. It was the back end of the medical consolidation that led to much of what we’re seeing today in the dental space. I would anticipate we’ll see much the same model play out in the dental space, which leads me squarely into my next point.

Junk Evaluations

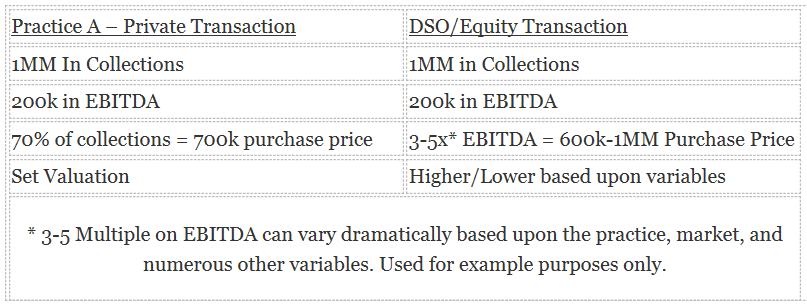

Evaluations are a dime a dozen. On the private practice side, almost every broker in the market is going to tell you that with minor variations, your practice value is roughly 70% of trailing 12 months collections. Collect a million, sell your practice for 700k. Pretty simple. On the investor driven side of it, they/we’re interested in purchasing profit dollars. Remember, there are investors to pay a coupon to, and debts that have to be paid. As such, the search for solid EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) is paramount and valuations on private practices are based entirely upon baseline EBITDA for that practice. So, to give you a little bit of insight, check out the following: In essence, the higher the quality level/profitability level of the underlying practice, the higher the valuation on the PE side. Why? Because profitability is what is valuable. Collections are devoid of value outside of the profitability that they lead to, which is why it’s so critically important to run a good business. In addition, the ability to prove long-term viability of the business and future sustainability of earnings are a key valuation point for any investor constituency.

In essence, the higher the quality level/profitability level of the underlying practice, the higher the valuation on the PE side. Why? Because profitability is what is valuable. Collections are devoid of value outside of the profitability that they lead to, which is why it’s so critically important to run a good business. In addition, the ability to prove long-term viability of the business and future sustainability of earnings are a key valuation point for any investor constituency.

All of that to say that we have a few interesting things on the horizon that are worth paying attention to.

DSO Equity Cycle

If you look back over the last 10-15 years and you track the equity cycles for several of the largest DSOs in the marketplace, you will notice that several large players are coming up on a time frame in which we’ll inevitably see an equity recapitalization. This often takes varying forms but will likely lead to few changes for most of the organizations and will provide additional capital to take the next steps in growth. Invariably, PE firms get smarter with every cycle they run through and we’re at a point now where much of the marketplace is pretty well informed when it comes to dental valuations and models that do and don’t work. I believe as we see this next round of changes, we’ll begin to see an evening out of valuations, along with a more rational and measured approach to acquisition strategies. Gone are the days when entities could dramatically overpay for assets. The piper needs to be paid and those poor investments are reverberating throughout the industry as I write this.

Grasping at EBITDA

Why do I see the market getting smarter? Quite simply there are currently too many poor evaluations. Often when an organization is at the end of their equity cycle, they attempt to grow EBITDA as quickly as they possibly can, prior to that recapitalization. The reasons are simple, however in layman’s terms, the more EBITDA you have, generally the higher the multiple you’ll demand on your recap. Obviously, there are a lot of other factors that play into this, however, for simplification purposes, we’ll leave it at that.

In many cases, this type of environment leads to poor purchasing decisions and inflated valuations on practices. Often many of these practices present operational difficulties long-term that may get overlooked with the full realization that the initial acquirers won’t have to deal with those problems. In addition, practices that aren’t necessarily a good fit get added to the group for profitability purposes with the understanding that both the profitability of the practice, and earn out due the seller (generally based on performance), will land at the feet of the next capital source who will essentially be left holding the bag trying to integrate these pieces and parts into the group. This commonly happens during the first or second cycle of PE involvement, however generally by the third cycle (where we’re in the midst of heading), most of the PE groups have gotten a bit wiser to the market and are more comfortable with specific parameters related to acquisition and valuation strategies. This has a calming effect on the market as a whole and cooler heads eventually prevail.

I believe we will begin to see a much more strategic acquisition protocol in the months/years ahead, with many of those acquisitions comprised not of private practicing owner doctors, but of group practices and small existing DSOs being consumed by their larger brethren.

Failure

When poor investment decisions are made, failure is an inevitability. In the midst of all of this consolidation and high valuation capital being tossed around, is the growing fear among some of the mid-tier DSOs that the private equity sources have gotten a little bit too smart. They’ve grown wise to practice metrics and, as mentioned above, are better versed in the art form of dentistry and practice management than the first couple of rounds of capital would indicate. As such, it is only a matter of time before we see one or more of these large DSOs left unable to recapitalize at the valuation they’ve promised shareholders, simply because of the value of the underlying assets.

I believe we are on the precipice of seeing one of the first major failures in the DSO space which will further shake valuations down the line. This will have a very interesting impact on both the dental capital markets and private practice bank financing, as some of these distressed assets are torn apart and debts are paid off.

Who’s Going Public?

Which leads me to my final thoughts. Who’s going public first? It’s going to happen, and I’m incredibly curious to see who it is, and how that impacts the marketplace. Modern wisdom would indicate it’s likely one of the big two or three that will make the jump. However, I wouldn’t put it past a lower Tier 1 group to look at the potential opportunities that a publicly-traded entity would provide in regards to a capital raise and the flexibility that might give them to make the jump into the top two or three (by market cap) in the country. That may be too tempting to pass up. Needless to say, that would usher in the next evolution in the dental space and would provide additional challenges to private practicing dentists.

In Closing

As the equity markets evolve, it should be reassuring to many that we’re still early on in the process. However, not so reassuring that you rest on your laurels. Larger amounts of capital necessitate bigger deals and our next phase of private financing will very likely focus less on private practicing dentist acquisition, and more on multi-site group practice and DSO acquisition strategy.

Connect with me on LinkedIn and feel free to comment or send me questions. I’ve been blessed to operate within this space for many years, and love to give back to the dental community! Have a fantastic week!

Josh Swearingen

Josh Swearingen

Director, Corporate Development

Joswearingen@amdpi.com

Connect on LinkedIn

Read Josh’s other articles here:

• From Scale to Sale: 5 Tips to Maximize the Value of Your Group Practice & Ensure it is Scaled for Success

• The One-Stop Shop Delivery Model – This is Just the Beginning

Looking for a Job? Looking to Fill a Job? JoinDSO.com can help: Subscribe for free to the most-read and respected

Subscribe for free to the most-read and respected

resource for DSO analysis, news & events: Read what our subscribers & advertisers think of us:

Read what our subscribers & advertisers think of us: