The dental lab industry has been rapidly changing over the past two decades.

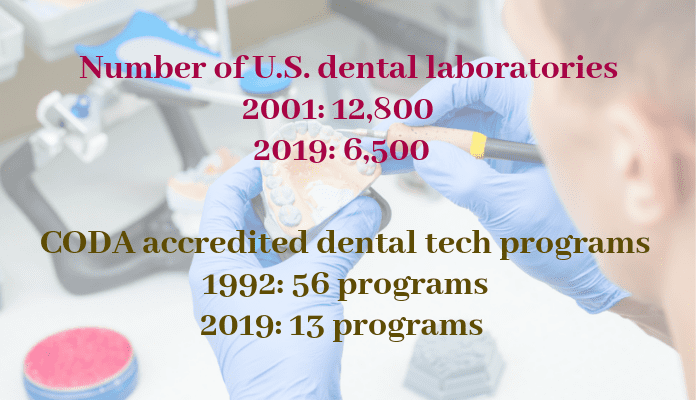

Firstly, the number of dental laboratories has declined dramatically. The National Association of Dental Laboratories (NADL), using data from the U.S. Department of Labor and Bureau of Labor, reflects a 22% percent decline in the number of U.S. dental labs with multiple employees — from 7,800 in 2004 to 6,100 today. However, the largest drop, has been in the category of sole-proprietor labs.

Bennett Napier, chief staff executive, NADL

“There was a time when there were almost 5,000 one person dental laboratories run by sole proprietors. Not all of those individuals have left the profession, some were acquired by other small to mid-size laboratories, or decided to become an employee of another laboratory. However, there were certainly a number of the one person laboratories coming out of the last recession that closed their doors due to economic conditions” -Bennett Napier, CAE, chief staff executive, NADL

Today, the NADL estimates there are only a few hundred sole-proprietor labs remaining. This reduction, mostly in smaller labs, is due to several factors:

1. An aging ownership demographic (much like demographics we see with dental providers) has led to an increasing number of lab sales and consolidations.

2. The proliferation of new technology required many lab owners to make capital expenditures to provide the new products and materials their clients were demanding. If lab owners decided not to make these capital investments, they chose to exit.

3. Technology also increased competition by making it easier for dentists to work with labs anywhere in the world, as opposed to working with a local lab.

4. The economic recession in the late 2000s, coupled with the rapid rise in the price of gold, led to a rise in the amount of work sent to offshore laboratories. That percentage of work done offshore by laboratories peaked at @45% a few years ago. While it has come down, around 35% of lab work sold in the U.S. still comes from outside the country.

While the number of dental labs has decreased, the number of U.S. lab workers has seen only a slight decline — from around 47,000 in 2001 to 46,000 in 2018. Even though there are fewer dental laboratories, demand for services has increased and dental laboratories have been able to meet demand through increased capacity due to the integration of technology such as CAD/CAM systems, digital files received from IOS, 3D printing, and more.

The changing dental laboratory industry has also impacted practitioners. Now more than ever, dentists (whether in a small practice or DSO environment) must be aware of the quality of their dental labs.

Travis Zick, NADL President

“Traditionally, general dentistry practices tended to do business with a local lab in order to get personal service. This led to a high number of small labs around the country that provided service to practices in a close proximity. Often, the owner also was the lead technician, or even the only technician. The utilization of technology in domestic labs, combined with new, man-made materials, has meant greater opportunity for American dentists to get competitively priced products domestically.” -Travis Zick, NADL President, Co-Founder, VP/COO of Apex Dental Laboratory Group, Inc.

In the past, dental labs were often viewed as order takers or prescription fillers, much like a pharmacy. “The role of today’s dental lab is so much different. The service and value a lab can bring is much higher than it has ever been,” said Zick. “For example, labs today can better assist with complex case planning. With the help of technology, we are able to work collaboratively through a full-mouth case with our clients to ensure a positive outcome at each step of the process — and much more quickly than in the past, when every step was done by hand.”

Technical Training

Since the 1970s, more than 27,000 dental technicians have graduated from formal dental laboratory technology schools. In 1992 there were 56 CODA accredited dental technology programs across the country. Today, the U.S. has only 13 accredited DLT programs. Accredited programs can only produce a graduating class of around 300 students each year.

Reversing the trend of school closures is extremely important to the future of the lab profession. In order to be successful in the dental relationship, a comprehensive foundation of knowledge is necessary, now more than ever. As a byproduct of school closures, dental laboratories have worked to create in-house training programs for new hires.

Technology Trends

The proliferation of technology, both in terms of dental materials and equipment in dentistry, and even more on the laboratory side, makes it crucial that there is open and consistent communication between the dentist and dental technician.

Dental technicians, by and large, work closely with dental manufacturers on the development of new restorative materials as well as the capital equipment that allows manufacturing of the substructure or the full restoration to meet the dentist’s need for the patient. Due to this dynamic, technicians and labs are poised to offer dentists expert guidance on material selection and help filter through the sales pitch on which brand is best to meet the patient’s need.

In addition, the rise in acceptance of digital impression systems has markedly improved the restorative outcome. In study after study, the detail of the digital file has facilitated both a better restoration and turnaround time. Remake percentages typically go down significantly both for the dentist and dental technician. This saves money, chair time and improves patient satisfaction.

It is important to share some statistical outcomes when dental laboratories and dentists use ISO systems:

Research from 2012 found non-digital GPs used between three-four labs (anterior, posterior, implants, esthetic cases). In comparison, IOS Digital GPs used between one-two labs for several reasons:

• Enhanced communication

• Consistency in impression receipt

• Consistency in returned restorative products and orthodontic appliances

• Consistency in price across multiple products and services

• Ability to shop a more complete digital portfolio of products and services

• Simplicity

Multiple research studies, including those published by the National Association of Dental Laboratories, indicate dental laboratories are one of the four primary resources for trusted information by dentists on materials and products

• Peers/colleagues

• Lab Technicians

• Trusted industry insiders/KOLs

• Journals, publications, social media from reputable sources

Dental laboratories were early adopters of digital technology, and mass utilization of new technology has occurred much faster in the dental laboratory market compared to the clinical setting. According to NADL research, 80% of the laboratory industry uses CAD/CAM as a primary manufacturing method for a wide range of products and services. 3D printing is a newer tool, but it has increased rapidly over the past two-three years with the introduction of new printing systems which are more reliable and accurate than those used in the past.

Because of the advantages of additive manufacturing, the integration of 3D printing by the majority of the dental laboratory market will likely occur in a ten to 12-year period, as compared to the 25 years it took for broader adoption of CAD/CAM.

Read Part 2 of this article here “Current Dental Laboratory

Market Trends & Their Impact on DSOs –

Part 2: Regulation & Competency”