Disclaimer: The opinions expressed within this article are solely the author’s and do not necessarily reflect the opinions and beliefs of this publisher/website or its affiliates.

In this article, Dr. Greg White, President and CEO of PepperPointe Partnerships, shares his insights on the state of the dental industry, providing perspective on the growth of DSOs, the impact of private equity in dentistry, and making predictions for the future. Dr. White is one of the founding partners of White, Greer and Maggard Orthodontics, which formed in 1991, and is currently part of one of the largest, independently owned pediatric and orthodontic Group Practices in the country. Prior to leading PepperPointe’s significant growth, he actively practiced orthodontics for nearly 30 years.

In this article, Dr. Greg White, President and CEO of PepperPointe Partnerships, shares his insights on the state of the dental industry, providing perspective on the growth of DSOs, the impact of private equity in dentistry, and making predictions for the future. Dr. White is one of the founding partners of White, Greer and Maggard Orthodontics, which formed in 1991, and is currently part of one of the largest, independently owned pediatric and orthodontic Group Practices in the country. Prior to leading PepperPointe’s significant growth, he actively practiced orthodontics for nearly 30 years.

The only constant in the dental industry lately seems to be change,

the largest change being rapid consolidation led by private equity,

marked with confusion and controversy.

The Tradition

The manner in which dental practices are transitioning has changed. For many decades, dental students graduated from their respective programs and started their own practices. They hung their shingle and began seeing patients and serving communities for their entire career. Others graduated and sought an opportunity to join a practice that was established. Typically they bought into that practice after an associateship period, eventually buying that doctor’s interest in the practice, maintaining the continuity of care for the patients in those communities for decades. Since the early-to-mid 1990s, there have been attempts to consolidate dentistry through dental service organizations (DSOs).

Since the early-to-mid 1990s, there have been attempts to consolidate dentistry through dental service organizations (DSOs). This concept of consolidation took on many different forms yielding mixed results. But, everything changed with the recession of 2008.

The Changing Events

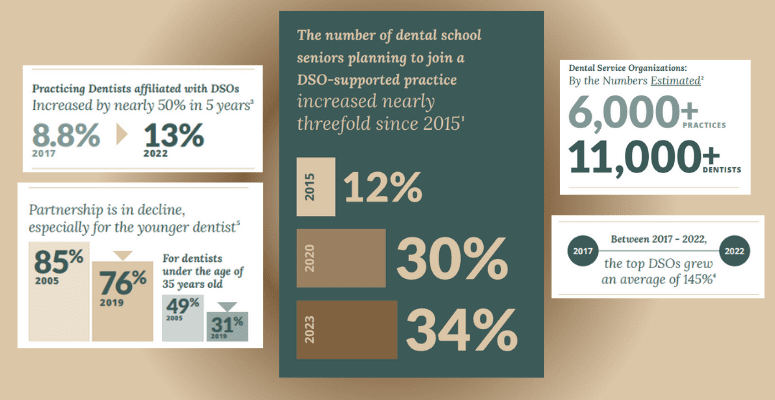

In 2008 the top and bottom lines of dental practices’ profit and loss statements began to suffer. Dentists, being conservative by nature, did what dentists do: they tried to save their way to prosperity. They searched for ways to cut costs and slowed efforts to grow the practices in the manner in which they had previously. The cost of dental education was on the rise leading to mounting debt, and access to capital was limited due to bank failures. The culmination of these events created a difficult climate for the new graduates to transition in the traditional manner. The result was fewer options for new graduates to work for existing practices. Some larger DSOs that formed in the early-to-mid 1990s saw this as an opportunity, which manifested in two different forms: there were practices available for purchase, and there were an abundance of available dental school graduates to hire and replace the doctors from the practices they were purchasing — fueling growth in DSOs (and overall general dentist practice consolidation) from roughly 2% in 2008 to about 13% in 2014.

The Financial Gap

These events created a financial gap between doctors seeking to sell their practice and retire (and the proceeds they wanted to receive for its sale) and the inability for the new graduates to pay that price. The DSOs took advantage of the opportunity. As the economy was recovering, a doctor wishing to sell his/her practi ce looked to the DSOs. Many doctors seeking employment upon graduating from dental school, with a substanti al amount of debt, found their best opportunity for employment was a DSO.

The Recent Proliferation of the DSO

In recent years, DSO growth has been fueled by the infusion of capital from private equity funds. Many factors led to the increase in PE involvement in dentistry over the last five years. The two greatest factors, from the provider’s perspective, are rooted in the feeling of isolation and the impact of the fear of missing out.

This is understandable when viewed from the dentist’s educational process. Business education is limited in the dental school curriculum, and doctors have limited time to devote to practice management. So, there has always been some struggle for doctors between their work as the practice manager and owner, and their work as the provider of treatment. This struggle has been exacerbated by the increased competition private equity-backed DSOs created, as well as difficulties for the provider related to COVID-19 and its ripple effect into supply shortages, labor issues, and record inflation. These challenges created fatigue and burnout for many, resulting in a surrender of valuable assets for a cash advance and entry-level pay going forward.

Many doctors don’t believe there’s another option but to sell, or they don’t believe there will be another financial opportunity as great as that of the private equity-backed DSO. They don’t want to miss out on this opportunity — an opportunity that has infiltrated conversations at every dental industry event. It’s expected (to some degree) as “celebrity dentists” share their experiences loudly and proudly. Dentists who authored dental school textbooks, dentists with large followings on social media, and podcast influencers are selling to DSOs and sharing their experience (and their big payouts). However, what many selling doctors don’t know is how different their paycheck will be relative to the celebrity dentists who are incentivized to a greater degree, including commissions for bringing others into a DSO.

Regardless, when doctors sell all future profits of their practices to private equity-backed DSOs it minimizes the opportunities for those professionals that follow, and it ultimately leaves the profession worse than we found it for patients, doctors, and communities.

Show Me The Money

You may be asking yourself, “Where are the DSOs getting the money to make these types of purchases?” From 2008-2013 the source of funding was typically traditional lenders. But, private equity (PE) began to take a look at dentistry and its high profit margins. Profit margins of a typical orthodontic, pediatric dental, or general dental office range between 30% and 50%, which was (and is) very enticing to PE companies. They began reaching out to DSOs, and business arrangements were formed as PE funds were used to buy majority interest to control DSOs. This changed everything, as a PE firm typically only invests for a short time frame (between three and five years).

It’s important to note that PE funds invested into DSOs are not being utilized to pay doctors for their practices. Instead, DSOs borrow these funds, and pay them off at their next equity event (recapitalization). Until that time, thDe DSO is making interest-only payments on those loans used to buy the dental practices. Some of the cash flow that the doctor owner previously took in profits is used by the DSO to support the administrative work of the DSO platform, but most of the profits are reaped by the owners of the DSO, which is predominantly owned by its founders and the PE investors; the doctors are only small stakeholders.

The DSO at this point is taking the lion’s share of the profits that the doctor once received. But, make no mistake, the doctors are still doing all the work and generating all of the production.

As interest rates rise DSOs pay higher interest rates on the loans and there are less profits for them and the investor. Plain and simple, it is a leveraged buy-out and success is dependent upon fluctuati ons in the market. This is nothing new, but it’s new to denti stry. We have seen PE enter other health care industries like medicine and pharmacy, and we’ve seen the results. There’s a lot of money being made for certain individuals and investors, but at what cost, and to whom?

So, Who Really Owns the Practice?

In most states dentists must own their practices, and they may continue to own those practices to some extent within a DSO. Considering this, it’s important to understand that a dental practice is composed of two different forms of assets: clinical assets and non-clinical assets. Clinical assets are defined as the patients and their records. Non-clinical assets are defined as everything of monetary value (i.e., furniture, fixtures, equipment, accounts receivable, the office leases, and even the names of the practices), and of course the profits. The private equity-backed DSO is focused on buying a majority interest in the non-clinical assets of a practice. Doctors maintain ownership in the clinical assets, meaning they are responsible for the work (providing the services) and the liability for all services rendered and their patients.

So, the private equity-backed DSO holds all the cards, and all of the value in the dental practice. The amount of money a doctor receives upfront, the amount of non-clinical assets sold (i.e., percentage of ownership sold), and the ongoing salary doctors agree to work for all have a symbiotic relationship. The more income a doctor earns as a provider going forward, the less money they’ll receive upfront in cash.

DSOs will also offer doctors the opportunity to buy stock in the DSO, just like you have the opportunity to buy stock in IBM or Google. But, those doctors will not receive the lion’s share of the profits (as they once did) because a DSO’s acquisition of a practice includes purchasing all current and future profits.

As of 2021, Private Equity Firms Owned6 27 of the top DSOs.

The DSOs may even mandate in the original purchase agreement that the selling doctor cannot sell all of their stock at the first recapitalization. They may also convince some doctors that they have the opportunity to take advantage of multiple recapitalizations. This ensures providers stay in “indentured servitude” for more years — more years of not receiving profits they once benefited from. There may be a financial benefit to the stock, or there may not be. There isn’t certainty associated with the value of the stock in a future state, and there are many important factors out of the doctors’ control that impact the stock’s value.

It cannot be overstated that through this DSO practice transaction the doctor becomes a commodity, and all future doctors will work for much less compensation than that of their predecessors.

A Cash Advance

To illustrate the mechanics associated with a dental practice transaction with PE, let’s use the example of a $2 million practice with a $1 million overhead. In this practice the doctor owner is receiving $1 million a year in profits.

A DSO will structure the deal as a job offer of $300,000 year to work (instead of $1 million they were making), and ask them to produce the same results (or better). The DSO will apply a multiple to the difference between the $300,000 and the $1 million to determine the value of the practice. A five multiple would provide for a $3.5 million valuation.

The DSO will offer the doctor $3 million in cash and $500,000 in stock in the DSO. After federal capital gains taxes, the doctor will have a balance of $2.4 million (minus state taxes, if applicable), but they are giving up $700,000 a year in income, and enter into an employment agreement for $300,000/year until the PE investor sells the majority interest and control of the DSO to another PE investor (approximately three-to-five years later).

For a period of roughly four years, the doctor gives up $700,000 a year in income ($2.8 million over four years). The dentist received $3 million in upfront cash, yet gave up $2.8 million over a four year period (but still did the same job for those four years). Some of the cash flow that the doctor owner previously took in profits is used by the DSO to support the administrative work of the DSO platform, but most of the profits are reaped by the owners of the DSO, which is predominantly owned by its founders and the PE investors; the doctors are only small stakeholders. The doctor could’ve gone to a bank, borrowed $3 million, self-imposed the $700,000 pay cut on himself and at the end of four years, would have $2.8 million pre-tax dollars and would still own their practice and the $1 million/year income. Keep in mind when a doctor sells to a DSO, the doctor is still generating the profits — just not receiving them.

That employment agreement, and what they are having to work for over the next 3-5 years, makes all the difference in the world converting it from being a traditional sale to a cash advance.

And, what does it mean for the next generation of dentists when doctors within a DSO retire? They’re replaced by another doctor who will work for the same $300,000 in this example. This type of transaction subjects the next generation of dentists to work for entry-level income, and never provides an opportunity for true ownership in a practice. There are instances where DSO associates make a little more and get stock options. However, they will never receive the financial benefits that the original doctors received. It is the commoditization of the dentist.

The Result

How does private equity’s entrance in the dental space impact patient care, or does it? And, why does it all matter?

Well, the PE-backed DSOs have a much higher turnover rate than the traditional doctor/owner model did in years past. Associate doctors working for a private equity-backed DSO are — and forever will be — employees, and those doctors have a greater propensity to move from one DSO to the next based on their next opportunity.

Furthermore, there is no long-term commitment to a specific practice and community when the name and reputation aren’t on the line, and when doctors aren’t receiving the benefits (and profits) as that of a true owner. This lack of continuity of care cannot serve the patient well.

What about communities? If a doctor does not own the practice (and its non-clinical assets) and control the profitability of the practice, the likelihood of that doctor having the authority and ability to invest into the community diminishes significantly.

Without true ownership, the ability to allocate resources, and commit to the community in any meaningful way is curtailed, or even derailed. Once again, we’ve seen this before in medicine and pharmacy. As community hospitals began closing down and became regionalized, we saw devastating results: access to care became more difficult, and opportunities for doctors lessened.

A Prediction of the Future of Dentistry

With private equity investing more than $100 billion in our industry it will be impossible for any other manner of consolidation to win in any meaningful way. Where they win, PE investors will own the majority of the profits, and doctors will work for those companies as employees with minimal power and little-to-no control over the future of the company they work for. Private equity-backed DSOs siphon off today’s profits and those of future generations. The quality of health care is dictated and ultimately controlled by whoever controls the allocation of non-clinical assets, and thus the downward spiral begins — all in the name of enough is never enough.

However, group practices are also on the rise. Doctors are beginning to see one another as potential partners and collaborators, not competitors. Many of these newly-formed group practices are building to sell to a private equity-backed DSO, and they may receive a large cash advance for the effort. But, there is another category of group practice owners who are choosing to stay independent and are creating alternative models. They are realizing they don’t need private equity funds to be successful in the future.

That realization was true for all of the doctor owners within the PepperPointe Partnerships family. PepperPointe was born in 2017 out of necessity to create a platform that performed the same functions as DSOs, but kept the ownership of clinical and non-clinical assets in the hands of the doctors. The PepperPointe model and platform is one in which PepperPointe doesn’t own the Group Practices it helps establish — each of our Group Practices are completely owned by their doctors. Therefore, all owners (doctor owners) are the decision makers of their Group. They continue to manage their individual offices with the opportunity to benefit from the success of the Group, and stay committed to their patients.

Our doctor owners do not relinquish equity in the operating business. They, by coming together, create a Group Practice (of which their individual practice is part of) that they, along with their doctor partners, own 100%. They receive all profits associated with their Group Practice. And, our Group Practices work in collaboration with the PepperPointe team to ensure their success and leverage all growth opportunities.

PepperPointe was founded on the principle that it will never sell to private equity, and its formation documents reflect that.

When doctors come together as owners to self-consolidate and leverage a platform like PepperPointe’s, they can increase their profitability and increase their income. A self-consolidated group of doctor owners creates an opportunity for the next generation of doctors by providing a pathway for them to become future owners of their group, which also provides a strategic exit plan for owners. This ownership opportunity ensures doctors’ long-term commitment to the group, thus reconstituting the traditional transition model, while preserving continuity of care for the patient. These doctors are motivated to invest in their communities. This commitment only occurs through the doctors having true 100% ownership and control of all aspects of the practice, clinical and non-clinical.

Self-consolidation provides for the best financial outcome for the selling dentist and the next generation of dentists by keeping profits (and all non-clinical assets) in the hands and control of dentists. It offers the best pathway for the transition from one generation of dentists to the next, and ensures continuity of care for the patients and commitment to communities.

Some group practices are realizing they don’t need PE. They are realizing they can leverage a platform like PepperPointe’s, while maintaining ownership in all the assets associated with their practice. The doctors are directly responsible and involved.

The problem is not DSOs; the problem is what the relationship is with the doctor. Specifically, the problem is who owns the DSO and who owns the non-clinical assets. Because of this, hybrid models and alternative options like the PepperPointe platform will continue to grow — platforms that help unite doctors without taking any of the ownership from the doctors. And, these models have the ability to yield the best financial results for doctors at all stages of their career.

For a model to be the best, three things are required: It must produce the best financial outcome for the exiting and entering doctor; it must be sustainable by creating a great transition from one generation to the next in an affordable fashion; and it must create the greatest alignment for all stakeholders: patients, doctors, and communities.

PE was left out of this list of stakeholders because they never have been considered one before. Who invited them to the party? Who will insist that they leave.

Sources:

- Istrate EC, Cooper BL, Singh, P, Gül G, West KP. (2023). Dentists of Tomorrow 2023: An Analysis of the Results of the 2023 ADEA Survey of U.S. Dental School Seniors Summary Report. American Dental Education Association (ADEA) Education Research Series, (Issue 6). Dentists of Tomorrow 2023: An Analysis of the Results of the 2023 ADEA Survey of U.S. Dental School Seniors Summary Report

- Association of Dental Support Organizations (ADSO) (n.d.). About the ADSO. ADSO. About the ADSO – Association of Dental Support Organizations || TheADSO.org

- American Dental Association (ADA) (2023, June 1). More dentists affi liating with DSOs. ADA News. Retrieved January 18, 2024, from More dentists affiliating with DSOs | American Dental Association (ada.org)

- Data obtained from DSO websites. Citations available upon request.

- American Dental Association (ADA) (2021, December 3). HPI Shifting practice patterns. New Dentist News. Retrieved January 18, 2024, from HPI Shifting practice patterns | American Dental Association (ada.org)

- Private Equity Stakeholder Project (PESP) (2022, March 12). Private Equity Health Care Acquisitions – January 2022. Private Equity Stakeholder Project. Retrieved January 18, 2024, from Private Equity Health Care Acquisitions – January 2022 – Private Equity Stakeholder Project PESP (pestakeholder.org)

Reprinted with permission of PepperPoint Parnterships